(Bloomberg) — As big tech companies raise hundreds of billions of dollars to fund artificial intelligence investments, Wall Street banks are increasingly finding they have to trade more credit derivatives to keep doing business with the hyperscalers.

Most Read from Bloomberg

The surge in activity is creating an opportunity for hedge funds to profit from banks’ growing demand for these instruments.

Banks typically face limits on how much exposure they can have to a single company across loan portfolios and derivatives books. But so-called hyperscalers such as Meta Platforms Inc. and Alphabet Inc. are raising so much capital to fund their artificial-intelligence programs — they are estimated already to have borrowed more than $250 billion globally for AI — that banks may be starting to approach those limits.

That’s where credit derivatives come in: they let banks buy protection against a company defaulting on debt, reducing their exposure to a borrower. They can then lend the firm more, underwrite its debt and trade derivatives with it.

Banks are constantly buying and selling credit derivatives tied to hyperscalers as their exposure shifts. But they are generally purchasing protection, because the derivatives give them the capacity to win more lucrative fee business. Their demand has driven up the cost of protection on hyperscalers to unusually high levels relative to their credit ratings. And hedge funds are looking to profit by selling that protection that can look overpriced.

“It’s the best opportunity in AA credit default swaps in a very long time,” said Andrew Weinberg, portfolio manager at Saba Capital Management, referring to the opportunity to sell protection on highly rated hyperscalers at prices typically seen for smaller, lower rated companies. “You are dealing with an inefficient market.”

Take Meta credit default swaps. Five-year contracts traded on Friday at about 0.73 percentage point annually, meaning a hedge fund selling protection on $10 million of principal can collect $73,000. There’s relatively little risk: Meta is graded AA- by S&P Global Ratings and Aa3 by Moody’s Ratings, the fourth-highest level.

It’s far more lucrative than selling CDS tied to companies in the broader North American investment-grade index. Five-year default protection on $10 million of the index cost about $52,000 annually, and the index’s average rating is about BBB+, or four notches lower than Meta. Selling Meta CDS therefore can generate significantly higher returns with higher rated credit.

Read: AI Bubble Fears Are Creating New Derivatives: Credit Weekly

Wall Street dealers that facilitate such trades say much of the demand for hyperscaler CDS is coming from banks’ credit valuation adjustment — or CVA — desks, which manage hedging arrangements.

Bank of America Corp. is among the dealers seeing a surge in activity. Monthly notional volumes of hyperscaler CDS trading at the bank are up tenfold since the beginning of 2025, according to Matt Mandell, BofA’s head of US single-name CDS.

“Investors continue to look to buy hyperscaler CDS, and a lot of that does come from the CVA desks,” Mandell said in an interview. “They’re trying to avoid being constrained by credit limits.”

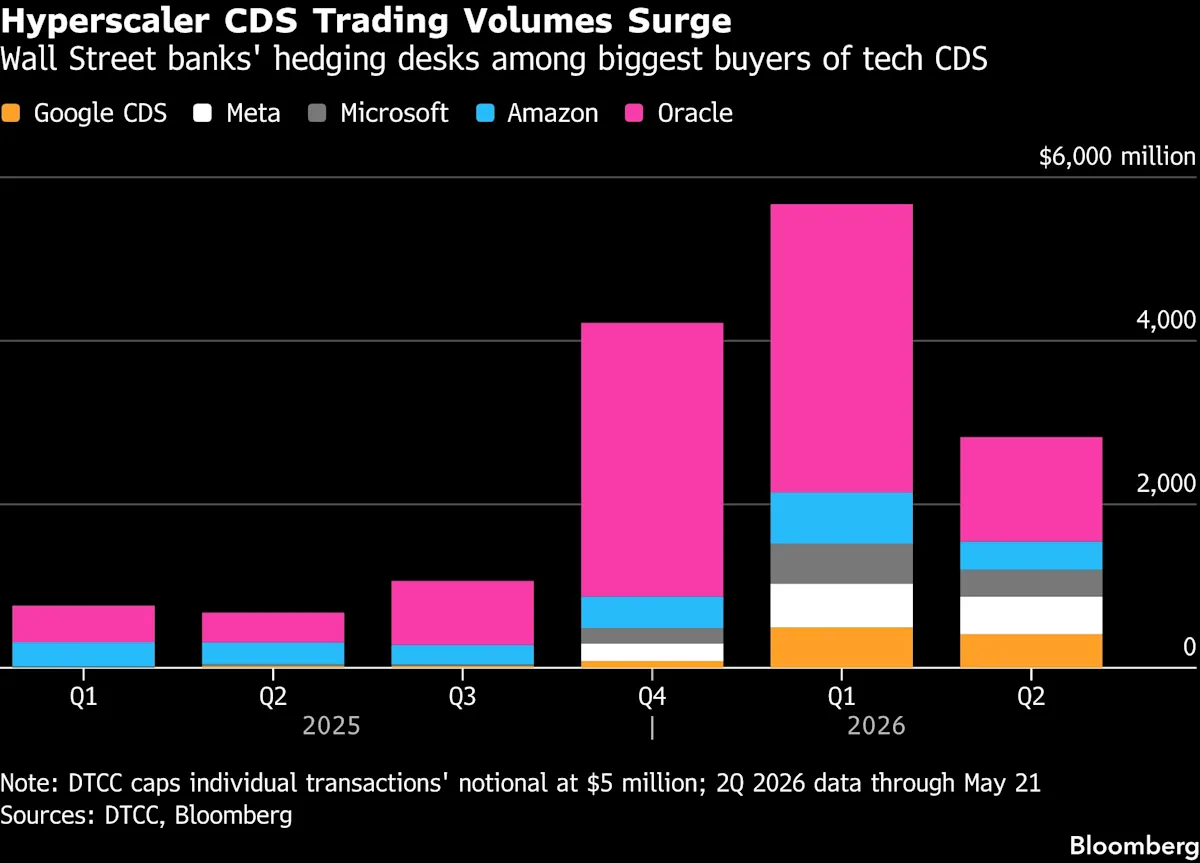

Bank demand is driving up prices for hyperscaler CDS, and pushing trading volumes to record highs.

CDS tied to Microsoft Corp., Amazon.com Inc. and Oracle Corp. notched $4.6 billion in notional trading volume in the first quarter, from $759 million a year earlier, according to Depository Trust & Clearing Corp. Meta CDS — only launched last October — had $534 million in notional trades, more than double the prior quarter. The figures likely understate activity because DTCC caps individual reported trades at $5 million.

Read: $300 Billion AI Debt Binge Spreads From Wall Street to Tokyo

With the artificial intelligence buildout projected to cost $5 trillion through 2030, CDS-selling hedge funds may have plenty more scope to profit.

For one, the debt spree is going global, with hyperscalers increasingly borrowing in currencies including euro, sterling and yen. That often forces CVA desks to buy more CDS, as companies often hedge foreign-currency exposure back to dollars through cross-currency swaps with banks. CDS can also help CVA desks hedge indirect exposure to data center deals and loans backed by graphics processing units.

“Banks are buying CDS to open up their credit lines, allowing them to trade and lend even more with hyperscalers,” Bofa’s Mandell said.

Demand is coming from other places too. Mandell is seeing more equity investors buy hyperscaler CDS as a cost-effective way to hedge stock positions. Asset managers and private credit funds are trading CDS on the companies as well.

Meanwhile, S&P Dow Jones Indices has added Meta, Alphabet and Microsoft to its CDX Investment-Grade Index, and JPMorgan Chase & Co. recently introduced a CDS basket that traders can use to bet against five hyperscalers’ debt.

Morgan Stanley strategists Vishwas Patkar and Joyce Jiang say there’s good risk-reward in buying protection on hyperscalers versus the broader investment-grade CDX index. While accepting that big tech firms are exceptionally high-quality, they say surging debt supply is concentrating exposure across a small set of issuers.

“Quality deterioration remains a risk,” they wrote in a note. “We like funding these shorts by selling protection on the broader index, which has less exposure to technology names.”

Listen to a podcast with Principal Asset Management about blue-chip firms risking their credit scores by piling on debt.

Week In Review

-

Yields on the US Treasury’s longest-dated bond rose to the highest level in almost two decades as investor concerns mount that accelerating inflation will force central bankers to raise interest rates. Higher yields are helping to spur companies to borrow before funding grows even more expensive: issuers poured into Europe’s bond market at the fastest pace ever on Tuesday, beating a record set just this month.

-

Bank of America and Citigroup are talking to investors about the makeup of the debt package financing Paramount Skydance’s acquisition of Warner Bros. Discovery Inc. Early conversations include about $30 billion of high-grade bonds and $12 billion of junk bonds, along with loans.

-

A JPMorgan Chase & Co.-led bank group is selling $10.2 billion of Warner Bros. Discovery loans, a figure boosted amid string demand.

-

Warner Bros. is pressing bondholders to exchange their securities for new junior notes secured by combined Warner Bros. and Paramount assets. Investors have until May 26 to decide.

-

Borrowing tied to the AI data-center boom is quickly climbing Wall Street’s list of potential credit threats, as investors increasingly worry that the breakneck pace of financing could sow the seeds of the next market shock.

-

China Evergrande’s liquidators are seeking 57 billion yuan ($8.4 billion) in their lawsuit against PricewaterhouseCoopers and its mainland China and Hong Kong affiliates, among the largest corporate claims ever sought in the city.

-

One of Switzerland’s largest pension funds, Publica, plans to invest up to $1.1 billion in direct lending, highlighting growing demand among retirement institutions for higher-yielding private-market assets.

-

Elon Musk’s reshaping of SpaceX, xAI and X into a tightly-bound conglomerate has already yielded a significant financial windfall: nearly $1 billion in annual interest savings, according to documents file ahead of SpaceX’s IPO.

-

The United States Tennis Association is in talks to borrow at least $400 million of private credit from institutional investors to refurbish New York’s Arthur Ashe Stadium.

-

LIV Golf has begun laying the groundwork for a potential US bankruptcy filing if it fails to raise new funds.

-

Optimum Communications, formerly known as Altice USA, is negotiating a new financing deal that could dilute the collateral backing its existing debt, potentially escalating a feud with a group of creditors it sued last year.

-

Raizen SA is considering pushing ahead with a debt restructuring plan over the objections of offshore bondholders, calculating that it has enough backing from bank creditors and local noteholders to win majority support.

On the Move

-

Canadian Imperial Bank of Commerce hired veteran banker Anvar Hodjaev to lead its US loan syndication business. Hodjaev most recently worked as a managing director at Mizuho Financial. CIBC has also hired Bank of America veteran Jeff Fritsche as global head of leveraged finance capital markets.

-

King Street Capital Management’s former head of capital markets Noah Charney has left the firm.

-

Credit-market veteran Naz Majidi is launching a new advisory firm to help asset managers tap fund finance, a market worth more than $1 trillion. Majidi was most recently a senior managing director at GreensLedge Capital Markets.

-

KKR hired Morgan Stanley Investment Management’s Masahiro Shuto as a managing director and head of its Japan capital markets business. Shuto, who was previously president of Morgan Stanley’s investment arm in Japan, started at KKR earlier this month.

-

Crescent Capital Group is preparing to launch a new fund focused on the booming market in significant risk transfers after hiring a team of bank capital experts in recent months.

-

Clear Street is cutting more than 50 jobs and replacing its CEO, as the Wall Street brokerage firm pivots after abandoning a plan to go public earlier this year.

-

Schonfeld Strategic Advisors is expanding its credit business, adding two sub-strategies and recruiting multiple traders as it works to deploy its growing assets.

–With assistance from Dan Wilchins.

Most Read from Bloomberg Businessweek

©2026 Bloomberg L.P.