(Bloomberg) — Policymakers in the US and across the Group of Seven will probably keep interest rates steady this week while watching nervously for signs of higher energy costs fanning inflation.

Most Read from Bloomberg

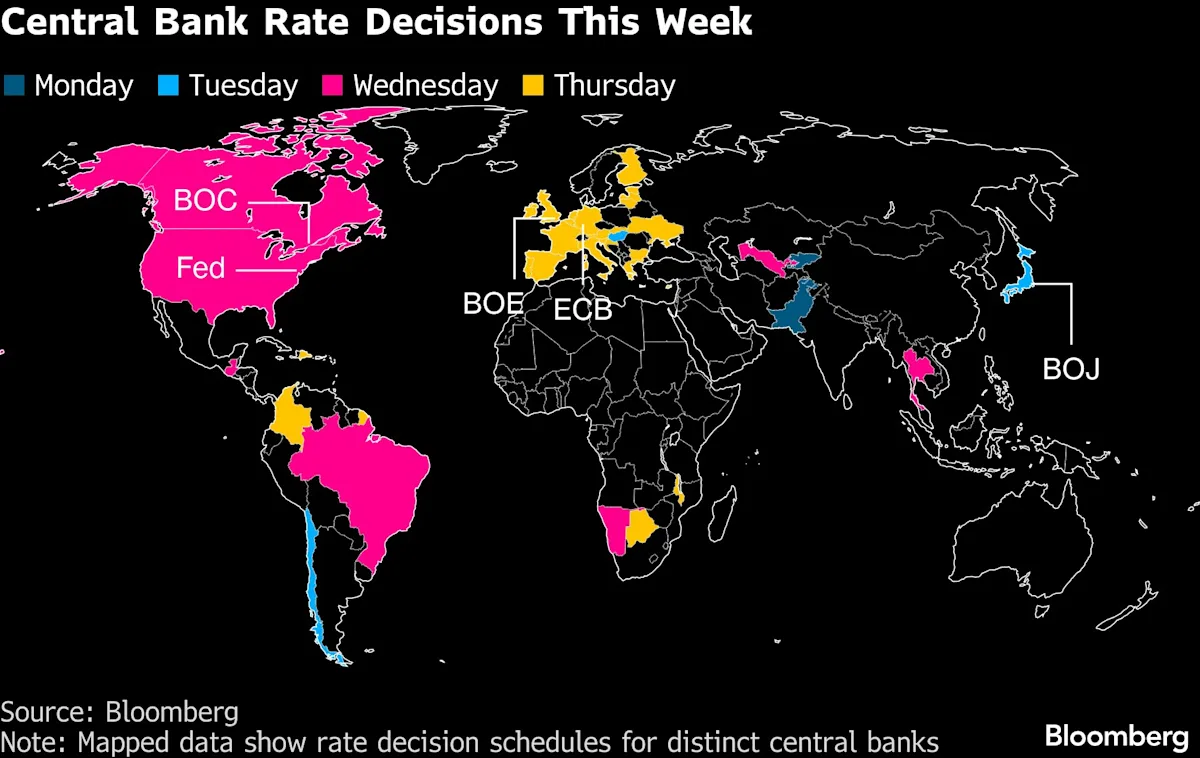

Three days of decisions in Washington, Ottawa, London, Frankfurt and Tokyo are widely anticipated to result in unchanged borrowing costs across the club of rich nations, with each central bank seen keeping a hawkish eye on fallout from the Iran war.

The combined outcome may amount to a firm reiteration by global monetary officials of their readiness to act. That posture would contrast with the sanguine approach prevailing at the onset of the last energy shock in 2022, when many viewed spiking inflation as transitory.

The Bank of Japan will be first on Tuesday, with officials who spoke in the past week leaning toward holding off this month on a potential hike.

The Bank of Canada and the Federal Reserve on Wednesday are both expected by economists and investors to insist on waiting and watching events too, and the Bank of England and European Central Bank will almost certainly echo with similar messages on Thursday.

While domestic conditions are key for all of them, events at the Strait of Hormuz, the Middle East pinch point of global energy supply, could well partly dictate the path of their monetary policy too.

Efforts to resume peace talks over the Iran war stalled after US President Donald Trump canceled a planned trip by his top envoys and the Islamic Republic said it won’t negotiate so long as it’s being threatened.

What Bloomberg Economics Says…

“In the week ahead, the Fed, ECB, BOE, BOJ, and BOC, among others, will probably leave policy rates unchanged amid persistent and volatile US-Iran tensions. We expect the Fed to hold rates steady until the fourth quarter, while the ECB and BOE keep the option to hike open.”

—Estelle Ou, economist. For full note, click here

The Fed policy meeting may well be the last for Jerome Powell as head of the US central bank.

The US Justice Department is ending an investigation into building-renovation cost overruns at the Fed, a move that led Senator Thom Tillis to say on Sunday that he’s dropping his blockade of the nomination of Kevin Warsh, Trump’s pick to take over from Powell.

Elsewhere, Chinese purchasing manager indexes, US and euro-zone inflation and growth numbers, and rate decisions from Brazil to Botswana will be on the schedule for investors.

Click here for what happened last week and below is our wrap of what is coming up in the global economy.

US and Canada

In the US, the economy probably accelerated at the start of the year, rebounding from a government-shutdown-driven slump at the end of 2025.

The initial snapshot of first-quarter gross domestic product is expected to show a 2.2% annualized advance, economists project ahead of figures due Thursday, helped by vigorous business investment. Consumer spending growth is forecast to soften slightly.

Separate monthly data from the Bureau of Economic Analysis, also out Thursday, are expected to show the initial impact on spending and inflation from the war in the Middle East.

Personal spending, adjusted for changes in prices, is expected to pick up slightly in March from a month earlier. The report may also show that inflation, measured by the Fed’s preferred measure — the personal consumption expenditure price index — accelerated to the fastest pace since 2023 on a year-over-year basis.

Excluding food and energy, the annual price gauge also probably quickened. The effective shutdown of the Strait of Hormuz has reduced the region’s exports of oil and other critical manufacturing materials — driving oil and other input costs higher.

Against that inflationary backdrop, and with the job market and economy showing few signs of a substantial weakening, Fed officials are widely projected to keep rates unchanged at the conclusion of two days of deliberations on Wednesday.

What Bloomberg Economics Says:

“The inflation impact from the Iran war will show up in the Fed’s preferred price gauge in the coming week, and the Fed will be on high alert for any sign that inflation expectations are losing their mooring. So far, they appear to be anchored.”

—Anna Wong, Stuart Paul, Eliza Winger, Chris G. Collins and Troy Durie. For full analysis, click here

The economic data-heavy week will also include separate reports on March housing starts and durable goods on Wednesday, as well as the Institute for Supply Management’s April manufacturing survey, due Friday.

The Bank of Canada is widely expected to keep its rate at 2.25%, with inflation near target and policymakers seeking more evidence on how the war-driven oil shock will shape price pressures and growth. The central bank will also publish updated economic projections, though it is likely to emphasize greater-than-usual uncertainty around its outlook.

Prime Minister Mark Carney’s government is set to release a mini-budget outlining revised expectations for deficits, revenues and bond issuance, along with new measures aimed at boosting investment and supporting workers affected by US tariffs.

Meanwhile, GDP data by industry for February and a flash estimate for March are expected to show only meager first-quarter growth as trade uncertainty and geopolitical tensions continue to weigh on the economy.

Asia

Asia’s calendar this week is headlined by the Bank of Japan’s policy decision, with a majority of economists still expecting the next rate increase in June. Expectations for an earlier move have faded as the US-Israeli war on Iran pushed up oil and gas prices, raising concerns about the impact on Japan, which relies heavily on energy imports.

The week begins Monday with China’s industrial profits, offering a read on whether stronger activity is feeding through to corporate earnings. Thailand reports car sales, Singapore releases industrial production and Pakistan’s central bank is set to decide rates, currently at 10.5%.

On Tuesday, South Korea publishes business surveys and New Zealand reports March filled jobs data. Japan’s labor market data and machine-tool orders will be in focus ahead of the BOJ decision.

Wednesday is the busiest day of the week. China’s official PMIs will be closely watched for signs of momentum heading into the second quarter, following the release of such surveys elsewhere. Japan reports retail sales and industrial production the same day.

Australia releases first-quarter inflation — a key reading for the Reserve Bank after back-to-back rate hikes — with markets returning from a Monday public holiday. Thailand’s central bank also meets to set policy.

Thursday brings China’s Caixin manufacturing PMI. Japan releases housing starts and consumer confidence, alongside Thailand’s current-account figures. Australia publishes private-sector credit and trade price indexes.

Friday rounds out the week with Tokyo inflation, a key leading indicator for nationwide price trends, alongside manufacturing PMIs across the region.

South Korea’s trade data will offer a timely gauge of global demand, while Australia and New Zealand release monthly house price figures for April.

Europe, Middle East, Africa

A shortened week before national holidays on Friday for much of the region will still offer plenty for investors to chew on.

In the euro zone on Wednesday, German inflation numbers are anticipated to reveal further acceleration caused by the fuel-supply crunch stemming from the Iran war.

Data for the whole region arrive on Thursday, with a jump in consumer-price growth to 3% expected. That would be the most since late 2023 and well above the ECB’s 2% target.

The same day, initial readings of GDP are expected to reveal growth holding steady at 0.2% in the euro zone, with expansion in every large country, but led as usual by Spain. While the numbers will cover the first month of the war, the effect of the conflict is more likely to weigh on momentum subsequent to that period.

The region-wide statistics will arrive shortly before the outcome of the ECB’s decision, where officials may defer the the prospect of a possible rate hike to their following meeting in June, when they will have new quarterly forecasts to hand.

The BOE’s announcement will arrive shortly before that of the euro zone on Thursday. Any switch in guidance will focus investors, given how the war is likely to have both stoked inflation pressures and hurt growth prospects. Markets will also watch to see if any official voted for a rate hike, with Chief Economist Huw Pill seen as the most likely candidate.

Other monetary meetings are also scheduled across the region:

-

In Hungary on Tuesday, the central bank will probably keep borrowing costs unchanged in its first decision since a watershed election installed a new government with its newly stated aim to pursue membership of the euro.

-

With inflation subdued, Namibia is likely to keep its benchmark at 6.5% on Wednesday as policymakers gauge the impact of rising global food and oil prices.

-

On Thursday in Botswana, where real rates have turned negative as fuel costs push inflation higher, the central bank is expected to tread cautiously. A weak backdrop may temper demand-driven price pressures, reducing the urgency for a hike.

-

Malawi’s central bank may hold its key rate at 24% as it assesses inflation fallout from the war. The southern African nation is already weighing the sale of gold reserves to ease a deepening fuel crisis.

-

Ukrainian officials may keep their own monetary settings steady the same day.

Latin America

Chilean economists and traders expect the central bank on Tuesday to hold at 4.5% for a third straight meeting after energy prices and inflation expectations jumped.

Chile is especially exposed to the fallout of the Middle East conflict, given that it imports nearly all its fuels. Chile-watchers can also look forward to the usual end-of-month data dump, including unemployment, retail sales and copper production.

Brazil’s mid-month consumer price data likely took another leg up as the Iran war’s energy shock sends fuel costs higher. March monthly readings jumped 0.88% to push the annual print up to 4.14% while 2026 inflation expectations have surged 89 basis points to 4.8% since Feb. 27.

Banco Central do Brasil holds its third monetary policy meeting of 2026 after last month’s quarter-point cut.

Policymakers led by bank chief Gabriel Galipolo have room for maneuver, but the most recent central bank survey of economists sees a second straight quarter-point reduction to 14.5% given uncertainty over the Mideast conflict.

Mexico’s first-quarter flash output reading may show Latin America’s No. 2 economy slumped from a 0.9% quarter-on-quarter expansion in the last three months of 2025 to a near standstill amid the sustained weakness in manufacturing and flagging domestic demand.

In Colombia, the third of the week’s three rate decisions looks to be largely drama-free with local media reporting that Finance Minister German Avila said he’d be willing to return to the board — after he walked out of the March meeting.

Economists surveyed by Banco de la República expect a half-point hike to 11.75%, up from 9.25% at year-end 2025.

In Peru, preliminary analyst estimates have inflation in the capital Lima slowing after surging to a year-on-year 3.8% in March, driven in no small part by the 9.4% jump in energy prices.

–With assistance from Swati Pandey, Laura Dhillon Kane, Vince Golle, Monique Vanek, Robert Jameson and Mark Evans.

(Updates with Tillis dropping his blockade of Warsh as Fed chief in ninth paragraph)

Most Read from Bloomberg Businessweek

©2026 Bloomberg L.P.