(Bloomberg) — Economic policymakers are about to gather in Washington to assess the damage President Donald Trump’s war on Iran has caused to growth in the Middle East and beyond.

For many attendees of the International Monetary Fund and World Bank’s spring meetings, to be held April 13-18 in the US capital, the trip will bring a sense of déjà vu, after last year’s event was dominated by punitive trade tariffs — another shock brought on by Trump.

The 2026 edition is set to focus on reading the tea leaves of US-Iranian negotiations this weekend aimed at turning a two-week ceasefire into lasting peace, and on how governments and central banks can best support their economies without creating new problems.

Ahead of the meetings, which will be attended by finance ministers and central bankers from around the world, IMF chief Kristalina Georgieva warned that the international community is becoming less able to respond to shocks. Fiscal space is lacking, policies that protect one country may harm others, and great-power politics are more likely to fuel conflicts than resolve them.

“Buckle up” was the main advice she offered ahead of new economic forecasts to be published on Tuesday, along with a report on global financial stability. “Given the impact of the war, we are going to downgrade them.”

In January, world output was seen rising 3.3% this year, with expansions of 2.1% in the US, 1.4% in the euro zone and 5.4% across emerging Asia. Then, at the end of February, bombs started hitting Iran.

“The next couple of quarters are going to be essential to understand how much this has tested the resilience of some economies that were a bit in a muddle-through period before the war,” Ludovic Subran, chief economist at Allianz SE, told Bloomberg Television.

What already seems clear is that the ripple effects of Trump’s aggression and the mistrust it has sown will linger — even if the truce agreed to by the US and Iran holds up, peace is restored, and shipping through a key waterway returns to normal.

“This ceasefire has clearly removed the most extreme downside risk,” said Ewa Manthey, a commodities strategist at ING. “For this to be a true turning point, we would need to see sustained and uneventful flows through the Strait of Hormuz, not just the headlines about reopening.”

What Bloomberg Economics Says:

“Last year it was tariffs. This year it’s oil prices. Trump’s America First instincts are injecting significant volatility into the global economy. In the end, the tariff shock proved less severe than anticipated. It’s possible the Iran war shock will go in the same direction. As long as the Strait of Hormuz stays closed, though, oil prices will stay high, the blow to global growth will deepen, and the impulse to global inflation increase.”

—Tom Orlik, global chief economist. For more, click here

With top monetary policy officials in Washington, the central bank slate elsewhere looks thin. Still, economic indicators are due across regions, including Chinese and UK GDP prints and inflation readings from India to Nigeria to Argentina.

Click here for what happened in the past week, and below is our wrap of what’s coming up in the global economy.

US and Canada

Investors will receive the next installment of March US inflation data with the producer price index on Tuesday. Similar to the consumer price report, the measure of wholesale inflation will reflect the surge in energy prices during the first month of the Iran war.

Economists project the PPI rose 1.1% from a month earlier, which would be the largest increase in four years. In addition to crude oil and diesel, the PPI could also indicate how quickly and to what extent disrupted Middle East production is spreading to the US.

The report includes price changes for materials used in the early stages of the production process, such as metals, plastics, chemicals and fertilizer. Transportation services costs may also reflect the impact from higher fuel prices.

The core PPI, which excludes energy and food, is forecast to rise 0.4% for a second month, extending a stretch of heightened wholesale inflation pressures that dates back to late 2025.

Apart from the PPI, the relatively sparse economic data calendar includes a report on March existing-home sales that will probably underscore a languishing housing market.

Economists expect little change in contract closings, which largely reflect buying decisions from a month or two earlier. Mortgage rates approached 6% in late February before advancing sharply in March, when inflation fears spooked the bond market.

Turning north, Canada’s March data on existing home sales and housing starts will offer insight into how the Iran conflict’s economic shock may be deepening hesitation among buyers and builders. The Canadian Federation of Independent Business’s latest barometer will be watched for early signs of how the oil price spike is shaping sentiment and investment.

February releases of manufacturing sales, wholesale sales and international securities transactions will help round out the pre-war economic picture.

Asia

China grabs the spotlight Thursday with the release of data expected to show that the economy grew 4.8% year on year in the first quarter, comfortably within the 4.5%-5% targeted range for 2026.

Retail sales, industrial output and property investment statistics for March, due the same day, will show what sort of momentum there was heading into the second quarter, when there’s a risk that sliding global demand owing to the Middle East conflict could erode business activity. Malaysia and Singapore also release first-quarter GDP this week.

Australia publishes a pair of sentiment gauges on Tuesday. The business confidence index for March may reflect the impact of the Iran war after the measure turned negative in February. The consumer confidence index is also due. Two days later, Australia releases March labor statistics that are likely to influence expectations about the RBA’s next policy decision on May 5. A focus will be on whether jobs growth can stay relatively robust after strong gains in February.

India on Monday is expected to report that consumer inflation accelerated to 3.4% in March, the fastest in nearly a year, but still well below the Reserve Bank’s 4% medium-term target. Wholesale prices later in the week are likely to grow at the quickest pace in three years. Malaysia also releases inflation figures in the coming week, and trade statistics are due from China and India.

There are no rate decisions in Asia, but two events involving BOJ Governor Kazuo Ueda are worthy of note. Ueda on Monday delivers his final scheduled speech ahead of the April 28 decision, and will hold a press briefing in Washington after the IMF and G-20 meetings on Thursday.

Given Ueda’s commitment to thorough communication — and with pricing in the overnight swaps market indicating traders see a roughly 60% chance of a hike this month — the appearances may be a chance to alert the market if it’s off base in its thinking, or to offer a nod of assent.

Europe, Middle East, Africa

Almost the entire European Central Bank Governing Council is heading to DC for the IMF meetings, with President Christine Lagarde, Chief Economist Philip Lane and Executive Board members Isabel Schnabel and Piero Cipollone all set to speak.

Back in Europe, accounts of the ECB and Swiss National Bank’s March 19 decisions, when both central banks held rates steady, are due on Thursday. Investors will be seeing if the reports show any biases toward rate increases — in the case of Frankfurt — or taking borrowing costs negative — in Zurich.

The same day, a monthly GDP reading for the UK is likely to show growth of just 0.1% in February — the last print before the impact of the Iran war shows up in output data.

Inflation numbers are scheduled for Israel and Nigeria on Wednesday.

In the former, data are expected to show the monthly consumer-price reading jumped the most in five months in March, as its joint attacks with the US on Iran intensified. Economists expect the measure to climb to 0.5% in March from 0.2% in February. The year-on-year print is nonetheless expected to remain at about 2%, well in the middle of the central bank’s 1%-3% target range.

Nigerian March inflation data will the first reading of price growth in the West African nation since the start of the Iran war. Fuel costs jumped more than 40% last month, impacting transport fares and food prices. Still, base effects may result in the annual reading easing to 13.4% from 15.1%, according to Bloomberg Economics.

Latin America

On Tuesday, Argentina’s March consumer price data are likely to again underscore the limits of President Javier Milei’s inflation fighting strategy.

Analysts surveyed by the central bank see the monthly reading hitting 3% for the first time in a year, while the annual reading languishes above 30%.

Budget data due Thursday is all but certain to show that Argentina met the March fiscal target outlined in its program with the IMF, while Torcuato Di Tella University’s leading indicator continues to run hot and cold.

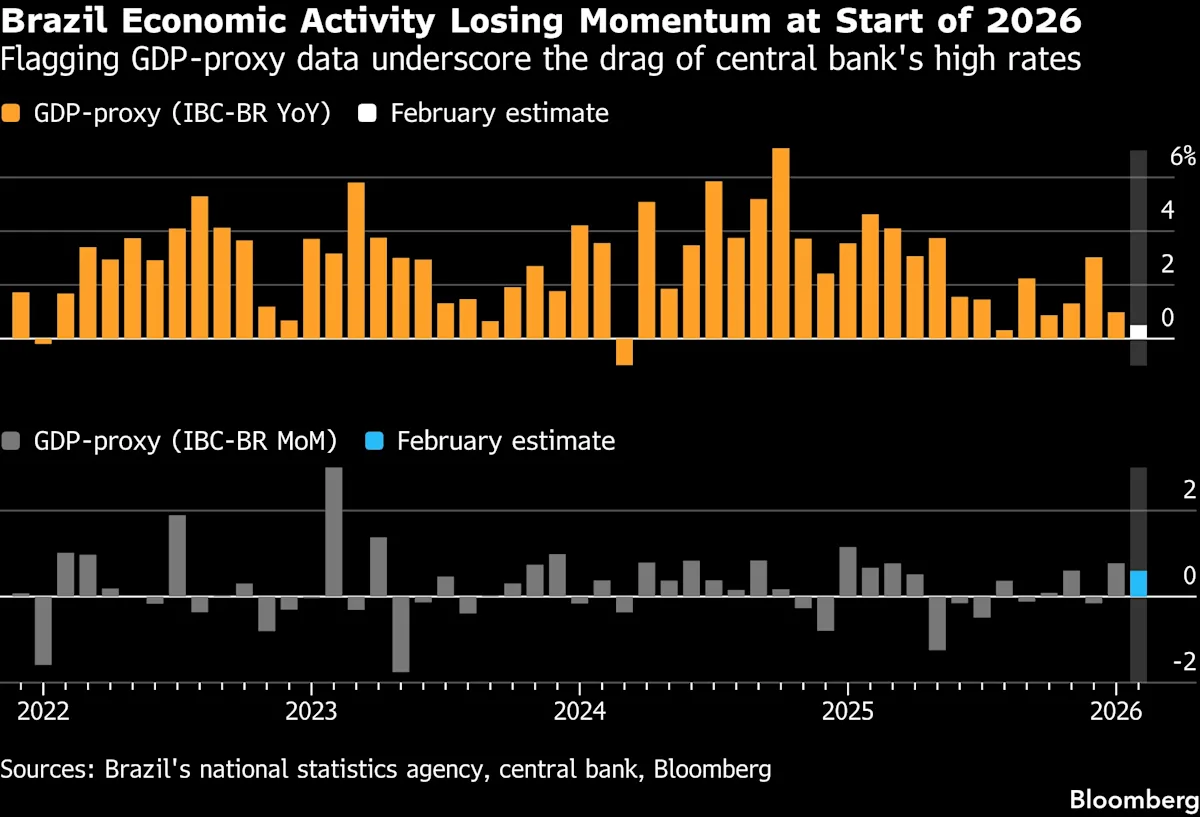

In Brazil, February GDP-proxy data look set to be more in line with an economy that’s flatlining under the weight of the central bank’s double-digit interest rates.

Ahead of elections this year, tax reforms, government transfers to low-income families, and steps to expand consumer credit will likely sustain consumer spending.

Banco Central do Brasil in March — before the US and Iran agreed the ceasefire — kept its 2026 GDP forecast at 1.6%, down from 2.3% last year. A prolonged Middle East conflict, the central bank had warned, would weigh on activity and spur inflation.

In the days after Sunday’s so-called mega ballot — the winnowing of more than 30 presidential hopefuls down to a final two for a June 7 run-off — Peru will report February economic activity as well as the March labor market report for the country’s capital of Lima.

Peru’s economy has been holding up, surprising analysts in the face of considerable political volatility; the nation’s had eight presidents and seven impeachment trials since 2016.

Still, January GDP-proxy data pointed to the cooling that most analysts see pulling 2026 growth below 3% from last year’s 3.4%.

–With assistance from Vince Golle, Simon Lee, Robert Jameson, Paul Richardson, Nduka Orjinmo, Lisa Abramowicz, Laura Dhillon Kane, Brian Fowler and Beril Akman.

More stories like this are available on bloomberg.com

©2026 Bloomberg L.P.