(Bloomberg) — A euro-zone interest-rate hike in the coming week is set to place the European Central Bank at the vanguard of global tightening caused by the Iran war.

Most Read from Bloomberg

The quarter-point increase expected for Thursday would be the most notable move so far, given that similar action in advanced economies has taken effect in much smaller jurisdictions, from Australia to Norway.

Unless ECB President Christine Lagarde and her colleagues challenge current investor bets, monetary policy will stay on track for further tightening, with at least one more hike penciled in for the remainder of the year.

While observers anticipate a similar trajectory from the Bank of Japan, which has a much lower benchmark, other Group of Seven central banks are far less inclined to raise borrowing costs at present.

On the eve of the ECB decision, the Bank of Canada may hold its own rate at the same level that’s prevailed since October. And later this month, both the US Federal Reserve and Bank of England are likely to keep settings unchanged as they watch the impact from the Iran conflict play out.

The response of officials in Frankfurt to the energy shock unleashed by US President Donald Trump’s attack on Iran will aim to ensure that the fastest euro-zone inflation since 2023 doesn’t become entrenched.

But their action will come at the cost of constriction to an economy whose underlying momentum was already feeble. The trade-off will become starker if policymakers persist with further tightening.

Different scenarios of how the shock might unfold in the region will be released, alongside quarterly forecasts. Lagarde will present those at a press conference following the decision.

What Bloomberg Economics Says:

“Lagarde may provide some indication of the ECB’s next move after she muddled communication on the rate outlook in March. We expect her to be clearer than in the past that a second hike may be in the pipeline.”

—Simona Delle Chiaie, chief euro-area economist. For full analysis, click here

Global stocktaking on the impact of the war may take hold elsewhere in the coming week, with data releases set to feature inflation gauges from the US to China and India.

Click here for what happened in the past week, and below is our wrap of what’s coming up in the global economy.

US and Canada

After job growth for May blew out forecasts in the US, the focus is back on inflation. The May consumer price index due on Wednesday is expected to jump by 4.2% from a year earlier — the highest rate in more than three years.

The core CPI measure, which excludes energy and food, is seen cooling slightly on a monthly basis, potentially providing a welcome signal to Fed policymakers. The producer price index on Thursday will offer further insight on the impact of the Iran conflict along the supply chain. Economists are watching the PPI report for components that feed into the the Fed’s preferred inflation gauge, the personal consumption expenditures price index, due later in the month.

Other reports in the coming week include May existing-home sales on Tuesday and the preliminary June consumer sentiment index from the University of Michigan on Friday. A blackout period for Fed officials kicked off Saturday ahead of new Fed Chairman Kevin Warsh’s first Federal Open Market Committee meeting, starting on June 16.

In an interview aired Sunday, Trump said that the Fed would be wrong to raise rates. Speaking with NBC’s Meet the Press, the US president sought to push back against market sentiment after the US jobs report spurred bets that the Fed’s next move will be a hike to keep inflation in check.

In Canada, the central bank is expected to hold its key rate at 2.25% for a fifth consecutive meeting as it balances an energy-driven rise in inflation against underlying economic weakness tied to US tariffs.

Wednesday’s decision won’t include updated economic projections, but Governor Tiff Macklem is expected to address data indicating Canada slipped into a recession in the first quarter while showing signs of a rebound in the second — including a surprise gain of 87,800 jobs in May. Meanwhile, April merchandise trade data are likely to show a widening trade surplus.

Asia

Asia’s data calendar will be dominated by updates on price trends.

China releases its May gauges for producer and consumer prices on Wednesday. Factory-gate price growth is seen accelerating to its fastest clip in almost four years, with Bloomberg Economics looking for 3.6% growth. Consumer prices are expected to advance more or less in line with the 1.2% pace in April.

India’s consumer inflation may continue to quicken in May on the back of food prices after the gauge accelerated in April to the fastest in a year, even as the government takes steps to keep a lid on fuel costs.

That would put added pressure on the Reserve Bank to consider a hike when the Monetary Policy Committee next sets policy on Aug. 5.

In Japan, with the central bank in a blackout period ahead of its policy meeting, decision, PPI data on Wednesday will likely show cost pressures on corporations remained elevated in May, after input prices rose in April at the fastest pace in 14 years.

That would further fuel expectations for a hike to the benchmark rate on June 16.

Hong Kong releases PPI statistics for the first quarter after the gauge rose the most since 2011 in the previous period.

In other data, Japan on Monday releases revised gross domestic product figures for the first quarter, with economists looking for a downward revision after fresh capital investment data for the period came in weaker than expected.

New Zealand’s manufacturing PMI for May is due Friday. The gauge has stayed in expansionary territory since July, but it’s slipped closer to the boom-or-bust 50 level in each of the past four months.

Sentiment surveys include consumer confidence readings in Indonesia and Thailand, along with the latest NAB Business Confidence gauge in Australia, which was mired well below minus 20 in March and April. Trade data are due during the week from Taiwan and China.

Meanwhile, investors will be keeping an eye on any moves from policymaker to support currencies across Asia amid heightened geopolitical tensions, rising energy costs and a stronger dollar.

South Korea on Sunday laid out a series of targeted measures to curb pressure on the won after the currency slid to its weakest level since 2009.

Europe, Middle East, Africa

Beyond the anticipated rate hike in the euro zone, national data may draw the most attention.

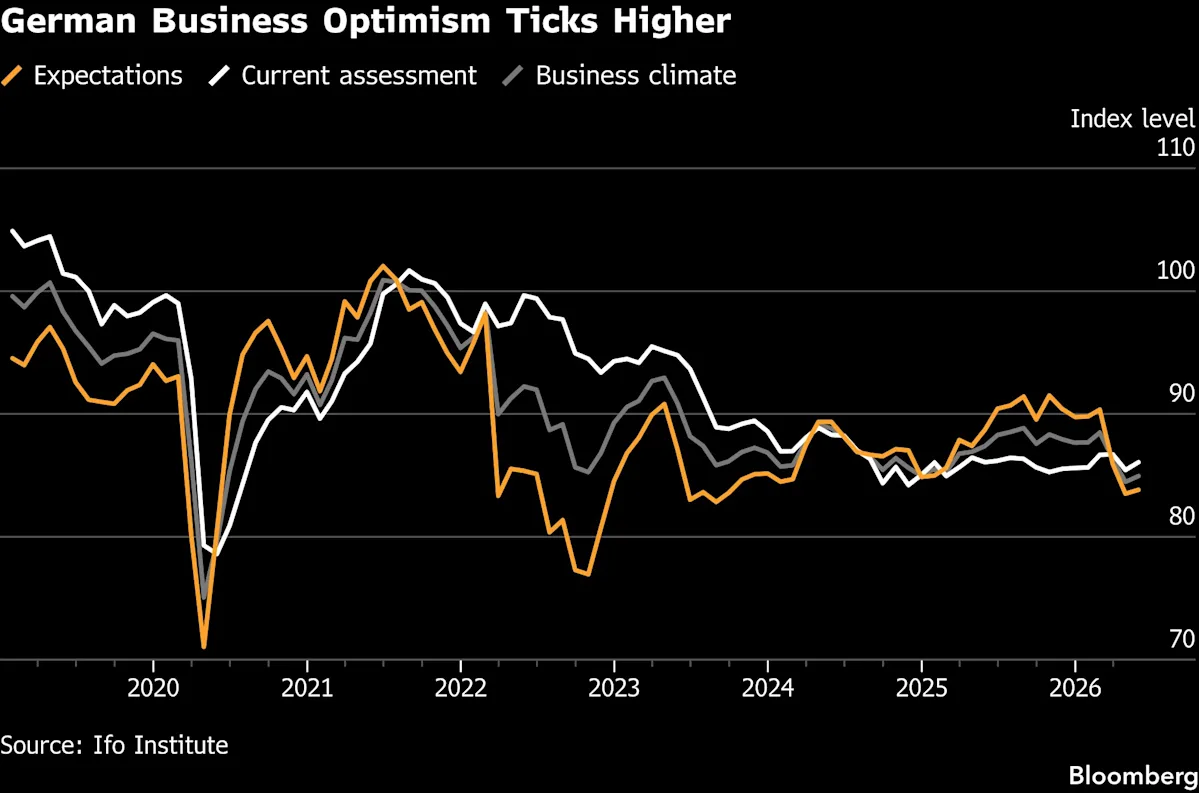

In Germany, factory orders on Monday, followed by industrial production and trade data on Tuesday, will illustrate the impact of the Iran war on the region’s biggest economy at the start of the second quarter.

The Bundesbank will issue new forecasts at the end of the week, when final inflation numbers will also arrive from Germany, France and Spain.

European finance ministers meet in Luxembourg on Thursday and Friday, gathering just after Brussels said it would give extra budget leeway to member states to cope with high energy prices stoked by the Iran war.

Italy, which had pushed for the change, on Sunday announced it would extend a fuel tax cut for consumers until July 3.

With BOE officials going quiet before their rate decision the following week, the UK focus will be on data. April GDP numbers will be published on Friday, with economists predicting the first contraction in eight months.

Turning north, inflation figures from Norway may show underlying price growth edged further above 3%. Concern at the strength of pressures there prompted Norges Bank to deliver its first rate hike since 2023.

Beyond the ECB, some other rate decisions are on the schedule in the region:

-

Kenya’s central bank is likely to keep its rate steady for a second meeting on Tuesday as it monitors the impact of the war. Inflation accelerated to 6.7% in May, the highest in two years and toward the upper end of the bank’s 2.5%-7.5% target band.

-

In Turkey, analysts are split on whether policymakers will hold rates steady or raise them on Thursday. Since the Iran conflict began, the central bank has paused funding from its policy rate of 37%, and switched to the costlier overnight lending rate of 40%. Still, May inflation is seen picking up to 32.5%, and officials may opt to deliver a hike to stem price pressures.

-

Serbia’s central bank will set borrowing costs the same day, revealing if it will continue to keep policy at the same level it’s been since 2024.

Latin America

Chile’s May inflation data posted Monday is likely to show the annual reading rose for a third month, pushing up above the 4% top of the central bank’s target range.

Consumer prices in April posted the biggest monthly rise since 2022 as the war in Iran pressures prices of oil — the Andean nation is especially exposed given that it imports nearly all its fuels.

Inflation readings from Mexico are due on Tuesday, the second-to-last consumer price reports available to policymakers before Banxico’s June rate setting meeting.

The early consensus suggests that the full-month print will slow to just above the 4% target range ceiling, while the bi-weekly reading may come in slightly below.

In Argentina, data for May will likely show that inflation accelerated more than 2% for a ninth month, pushing the year-on-year print up from April’s 32.4% reading.

Remarkably, inflation these days is no longer the dominant concern among Argentines — corruption and unemployment now top the their list of worries ahead of next year’s presidential election.

Peru’s central bank meets Thursday after the most recent annual inflation readings showed a slight cooling in May, although both the headline and core prints are running well above target.

Policymakers last month delivered a hawkish hold, signaling their readiness to raise rates. A quarter-point hike to 4.5% appears likely.

Closing out the week, Brazil’s benchmark IPCA inflation index likely pushed up over the 4.5% top of the central bank’s target range as food and electricity costs continue to move higher.

These are the last of the IPCA readings — the mid-month IPCA-15 report comes out June 25 — available to Brazil’s central bank before its June 16-17 rate setting meeting.

–With assistance from Brian Fowler, Laura Dhillon Kane, Robert Jameson, Mark Evans, Piotr Skolimowski, Cécile Daurat and Paul Richardson.

(Updates with Trump on Fed in US, Canada section)

Most Read from Bloomberg Businessweek

©2026 Bloomberg L.P.