(Bloomberg) — The Federal Reserve’s favored top-line inflation gauge is rapidly approaching 4% as a war-driven spike in energy costs generates unease that price pressures will broaden.

Most Read from Bloomberg

Government data on Thursday are expected to show the personal consumption expenditures price index jumped 3.8% in April from a year ago. That would put inflation a full percentage point higher than it was in February, marking the biggest two-month acceleration since late 2021.

Even stripping out energy and food, the so-called core price measure likely picked up in April to the fastest pace since late 2023.

The surge in prices for fuel and other materials created by the war in Iran is reverberating throughout the world economy, with consumer sentiment in the US tumbling to a record low and global businesses highlighting cost concerns. What’s more, inflation expectations are mounting, and bond yields are climbing.

In addition to the inflation data, several Fed officials are set to speak in the coming week, including John Williams, Philip Jefferson, Neel Kashkari and Alberto Musalem. Investors will parse their comments for any concern about the longer-term outlook for inflation given persistent supply constraints related to the Middle East conflict.

On Friday, Fed Governor Christopher Waller said he supports making clear that the central bank’s next interest-rate move is just as likely to be an increase as a cut.

In addition to the PCE price data, the Bureau of Economic Analysis’ report will include figures on personal spending and incomes. Those will offer an early peek into household demand at the start of the second quarter. Economists expect a modest increase in inflation-adjusted spending and a slowdown in the nominal growth of personal income.

Gasoline prices near the highest since 2022 are compounding Americans’ concerns about the cost of living. The toll of inflation on household budgets poses a risk to the spending outlook.

What Bloomberg Economics Says:

“If confidence weakens further, it would reinforce the risk that spending momentum softens into summer. The latest earnings for companies in the consumer-discretionary sector, such as Target, indicate that tax refunds have supported spending so far. If the Strait of Hormuz remains closed, sustained higher gas prices will erode the tax-refund cushion.”

—Anna Wong, Stuart Paul, Eliza Winger, Chris G. Collins, Alex Tanzi and Troy Durie. For full analysis, click here

On Thursday, the government will issue a revised first-quarter gross domestic product report that includes personal outlays for the period.

Among other economic data scheduled during a holiday-shortened week, the Conference Board will release its May consumer confidence index on Tuesday, while April durable goods orders and new-home sales are due on Thursday. At week’s end, the government will release figures on April merchandise trade.

In Canada, GDP by expenditure is expected to show a 1.5% expansion in the first quarter, reversing the 0.6% contraction recorded at the end of 2025. Governments, businesses and consumers all likely increased spending, though momentum for firms and households may have stalled late in the quarter as the oil shock hit.

Residential investment is expected to remain weak amid a sluggish housing market and flat population growth, while US tariffs continue to weigh on exports despite surging gold and crude shipments. The current account balance will offer important insight into foreign direct investment after inflows surged in the fourth quarter.

Meanwhile, Bank of Canada External Deputy Governor Nicolas Vincent will speak on labor-market trends and structural change in the economy, following a four-month string of job losses that was the steepest since 2021.

Elsewhere, inflation gauges in key economies from Australia to Germany and Brazil, and a likely rate increase in South Africa, will be among the highlights.

Click here for what happened in the past week, and below is our wrap of what’s coming up in the global economy.

Asia

Three Asia-Pacific central banks decide policy in the coming week, with the Bank of Korea holding its first board meeting under newly installed Governor Shin Hyun Song.

A key point there will be the six-month dot-plot. When introduced in February, the dot-plot indicated authorities were neutral on the outlook, as they expected to hold the rate steady for six months. That stance may shift as policymakers grapple with mounting inflation concerns.

The Reserve Bank of New Zealand is expected to hold its cash rate at 2.25% on Wednesday, with investors likely to focus on prospects for a move in July after near-term inflation expectations climbed in the first quarter to the highest since 2023. Sri Lanka’s central bank also decides policy.

Several nations will report on inflation. Singapore’s overall price growth is estimated to have accelerated to 2.1% in April after marking the fastest gains since 2024 in the previous month.

In Japan, Tokyo’s underlying inflation trend likely held mostly steady in May excluding distortions related to subsidies, giving the Bank of Japan room to mull a hike next month.

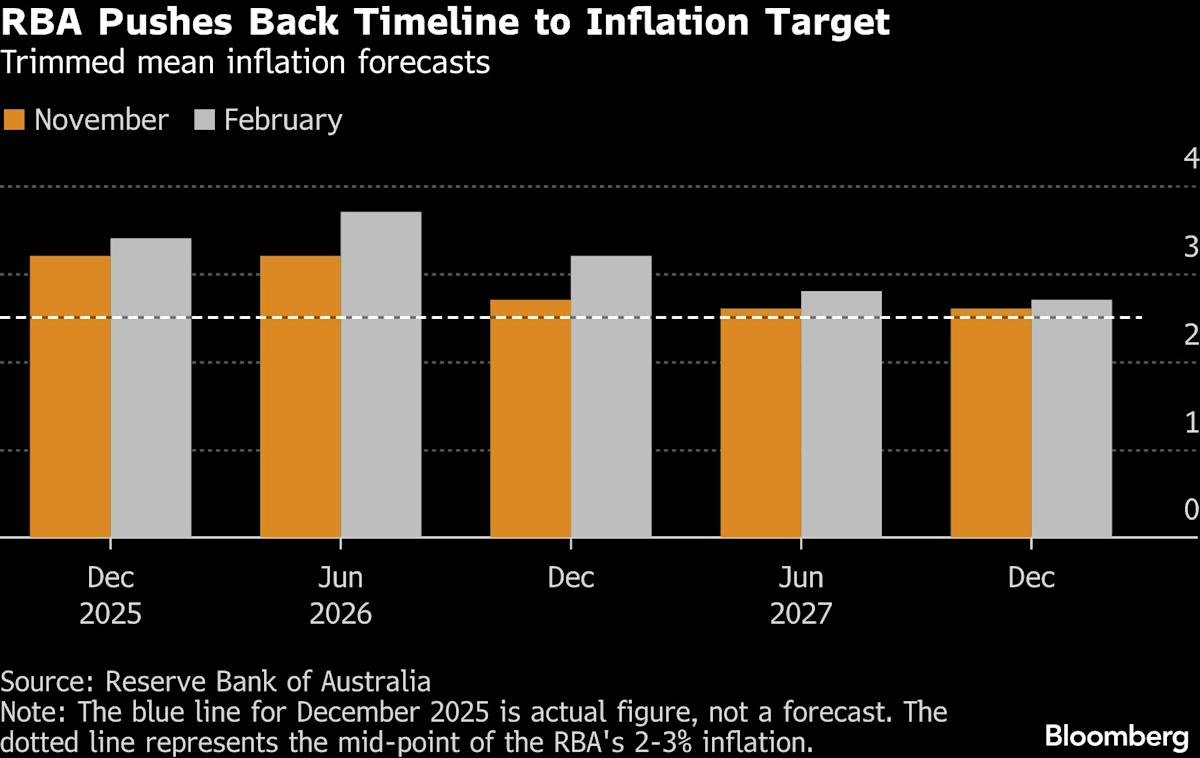

Australia’s CPI statistics due on Wednesday may show the closely-watched trimmed mean gauge staying above the central bank’s target band in April, keeping pressure on the RBA as traders project another rate hike in August or September.

China’s industrial profits for April will indicate how well manufacturers are coping with global geopolitical turbulence after they climbed 15.5% in the first quarter, the biggest gain for that period in five years.

New Zealand releases a pair of sentiment gauges on Friday. Consumer confidence for May comes after it fell to a three-year low in April. Business confidence may stay under pressure after slumping to its lowest since 2023 in the previous month.

Trade data are due during the week from the Philippines, Thailand and Hong Kong.

Europe, Middle East, Africa

A shorter week in Europe, with Monday a holiday in many countries, will still keep investors busy with several data releases and central bank events.

Friday is a highlight in the euro zone as inflation numbers from its four biggest economies are due. They may show faster consumer-price growth fueled by energy in France and Italy, with headline gauges in Germany and Spain holding at levels last seen in 2024.

That’ll feed into a reading for the region scheduled for release on June 2, the final measurement available to the European Central Bank before its meeting the following week.

Releases from the ECB include its Financial Stability Review on Wednesday and an account of its April rate decision the following day. Among appearances from officials, chief economist Philip Lane speaks in Tokyo on Thursday, and Bank of Italy Governor Fabio Panetta is set to deliver a key annual speech on Friday.

Speaking on the sidelines of a May 22-23 meeting of European finance chiefs in Nicosia, ECB Governing Council member Martin Kocher said that “everything points to us deciding between holding and raising rates — and it’s clear to me that if the situation doesn’t improve, we will have to focus our discussions on acting.”

Policymakers from multiple institutions will be out in force at a conference in Reykjavik starting on Thursday. Central-bank governors from several advanced economies are scheduled to attend, including Bank of England chief Andrew Bailey, his Norges Bank peer Ida Wolden Bache, and Swiss National Bank President Martin Schlegel.

Four other appearances from UK monetary officials are scheduled, with Deputy Governors Clare Lombardelli and Sarah Breeden speaking at separate events on Wednesday, and rate-setters Catherine Mann and Megan Greene participating in a conference in the Croatian port of Dubrovnik at the weekend.

In the Nordics, first-quarter GDP numbers will be released in Sweden, with a contraction likely, and Norway, where economists reckon growth held to a robust pace.

Turning east, Bulgaria’s new government is expected to take its first steps toward a budget bill after delays caused by the country’s political crisis.

Some monetary decisions are scheduled around the wider region:

-

Israel’s policymakers face a tough choice on Monday. Eight of 14 economists surveyed predict the Bank of Israel will cut its rate by a quarter point, to 3.75%, to give the war-hit economy some relief. Others see no change.

-

Also on Monday, Mozambique is expected to leave borrowing costs steady as officials gauge the inflation impact of soaring energy and food prices.

-

Hungary’s central bank is anticipated to keep rates on hold the next day, although some officials suggest a cut is on the cards as early as June.

-

On Thursday, South Africa is poised to join a handful of central banks in raising borrowing costs to contain the inflationary fallout from the Iran war. A quarter-point rate increase to 7% would be the first in three years.

-

That move in Africa’s largest economy will reverberate in neighboring Eswatini and Lesotho, whose currencies are pegged to the rand. Their own decisions come a day later.

Latin America

Brazil’s mid-month consumer price report is all but certain to show that inflation drifted higher, possibly breaching the 4.5% top of policymakers’ target range following April’s 4.37%.

Given that demand has played virtually no role in the recent run-up in consumer prices, though, the central bank may be comfortable in extending the current gradual course of easing at its next meeting in mid-June.

Uruguay’s central bank meets with inflation running below both the 4.5% target and 5.75% key rate. Bank chairman Guillermo Tolosa in late April said board members are taking a wait-and-see approach to monetary policy.

Four of the region’s big economies will post April labor market data, with figures from Peru — unemployment in the capital Lima hit 5.3% — already in.

The jobless rate in LatAm’s No. 1 economy pushed over 6% in March for the first time in 10 months, but there’s still little slack in Brazil’s labor market. Mexico’s streak of sub-3% unemployment prints may be running out of road as lower participation rates and rising informality point to weakness at the margins.

The war in Iran may see Banxico dial down some 2026 forecasts in its January-March inflation report — the 1.6% GDP estimate from the February publication is above the consensus, while the inflation projections strike many Mexico-watchers as overly optimistic.

Brazil’s first-quarter output report will likely show the nation shook off 2025’s second-half funk to notch a strong start to 2026.

Industry and manufacturing have stepped in as agricultural output has faltered, while household consumption continues to hold up, with new government tax and credit initiatives poised to help bolster demand heading into the October elections.

–With assistance from Piotr Skolimowski, Shamim Adam, Mark Evans, Brian Fowler, Monique Vanek, Robert Jameson, Laura Dhillon Kane and Paul Wallace.

(Updates with Kocher in EMEA section)

Most Read from Bloomberg Businessweek

©2026 Bloomberg L.P.