Meeting the Sustainable Development Goals requires trillions of dollars of investment in developing economies each year, far exceeding what official aid budgets can provide. The answer, according to a broad policy consensus, is blended finance: the deliberate use of concessional public money to crowd in much larger flows of private capital. Development finance institutions now deploy over $250 billion annually through these operations, roughly four times what they mobilised a decade ago.

Yet for all its prominence, blended finance rests on surprisingly thin analytical foundations, and while the grey literature on the topic is large, academic work is much more limited (Aydin et al. 2024, Flammer et al. 2024, Claessens and Kapoor 2026 are notable exceptions). Practitioners know that these instruments can mobilise private capital; they know far less about when they do so effectively, which instrument works best in which setting, and when a simpler direct grant would do more. In a new paper (Panizza 2026), I address these questions by developing a simple model of blended finance multipliers and deriving results that translate directly into operational guidance.

The multiplier: What it measures and why it matters

The central metric of the paper is the catalytic multiplier: the increase in total project size per dollar of expected public expenditure. A multiplier of three means that each dollar of public money generates two additional dollars of private investment. A multiplier of one means no private capital is mobilised at all: the entire increase in project size is accounted for by the public contribution itself. A multiplier below one is worse still: it signals that direct public involvement would have produced a larger investment response.

This is the metric that development finance institutions use in practice to rank interventions and report to donors. Understanding its determinants therefore has direct operational value.

I consider two canonical instruments — subsidised loans and credit guarantees — deployed to correct three types of market failure: production externalities (where entrepreneurs undervalue the social return of their investments), financial frictions (where the cost of capital is elevated by excessive risk premia, illiquidity, or insufficient banking competition), and credit rationing (where borrowers cannot access the full amount they need regardless of the interest rate they are willing to pay).

The fundamental tension at the heart of blended finance

The paper’s first result is that the catalytic multiplier is decreasing in the severity of the market failure. Interventions targeting the largest distortions achieve the lowest leverage. The mechanism is straightforward: correcting a large distortion requires a proportionally large subsidy relative to the induced investment, compressing the ratio of additional private capital to public expenditure. Economists know this: there is no private provision of pure public goods. The opposite also holds: high reported multipliers may instead reflect operations in markets that are nearly efficient to begin with (see Figure 1).

The practical implication is important. Agencies operating in highly distorted environments — precisely where the development need is greatest — should not expect high multipliers and should not be penalised for reporting modest ones.

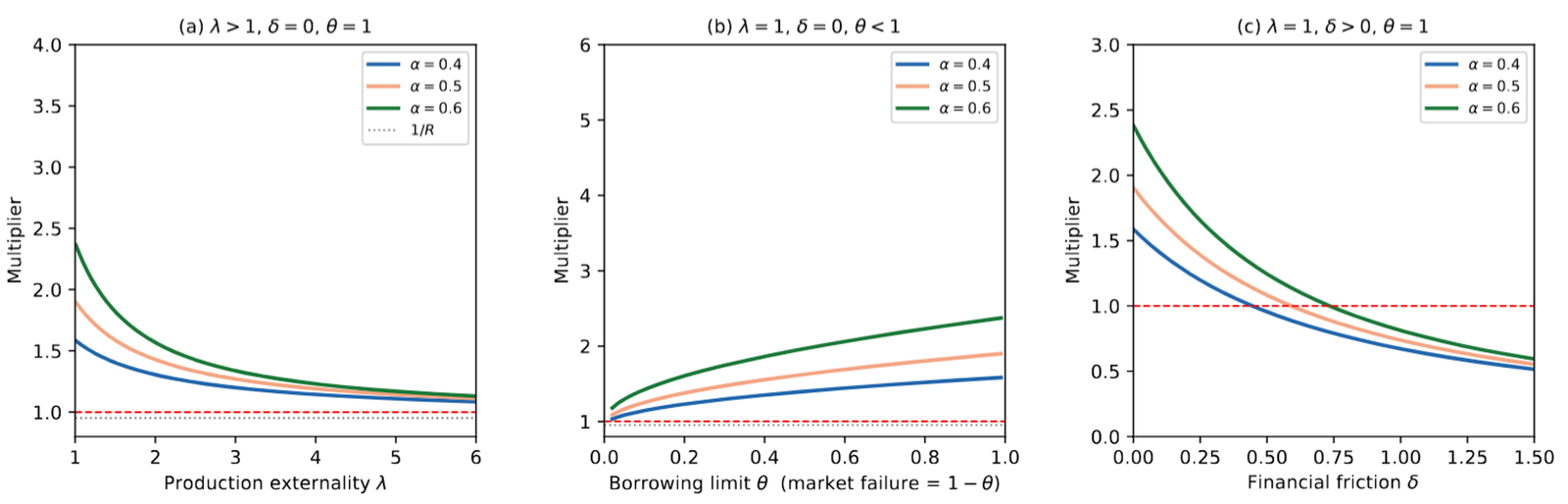

Figure 1 The catalytic multiplier of a subsidised loan and market failures

Notes: The left panel shows how the multipliers vary with production externalities (measured by the externality parameter λ). When λ is close to 1 there are limited production externalities — very small market failures — and the multiplier is large; as market failures increase, the multiplier decreases. The middle panel shows the effect of credit constraints (measured by θ, where θ = 1 means no credit constraints and θ = 0 means constraints are at their maximum). When θ = 1 the multiplier is large; when θ = 0 the multiplier falls to 1. The right panel shows the effects of financial frictions that increase borrowing costs (measured by δ). When financial frictions are absent (δ = 0) the multiplier is large; as financial frictions increase the multiplier decreases and can even fall below one.

Different types of de-risking

Blended finance interventions often focus on de-risking a given project. However, the concept of de-risking is often used loosely in policy discussions in ways that obscure two fundamentally different situations.

In the first situation, private investors perceive a project as risky when it genuinely is not — or at least far less so than their pricing implies. This might occur because lenders lack information about a new market, because regulatory constraints penalise emerging-market exposures regardless of actual credit quality, or simply because private capital has never flowed to a particular type of project before. The empirical evidence supports the prevalence of this phenomenon. The Global Emerging Markets Risk Database, which draws on over three decades of lending data from 29 multilateral development banks, documents an average default rate of 3.54% for loans to private entities in emerging markets alongside recovery rates that exceed global benchmarks (Chari et al. 2025). This suggests that investors are systematically pricing in risk that does not materialise.

In this case, a guarantee can be extraordinarily effective at close to zero fiscal cost. If the project is genuinely safe and the guarantee is rarely called, the public sector has mobilised private investment at almost no expense. This is the scenario where blended finance can achieve multipliers that are, in principle, unboundedly large.

The second situation is fundamentally different. Here, default risk is real. Projects in developing countries can and do fail; borrowers genuinely may not be able to repay. In this case, a guarantee that absorbs default risk has a real expected fiscal cost: the public sector is providing genuine insurance, not just correcting a misperception. The question then becomes whether absorbing that real default risk is worth the expense.

The paper shows that the answer is usually no, and that conflating the two situations leads to poor instrument choices.

For subsidised loans, the paper proves that interventions which address market failures while leaving default risk intact always achieve a higher multiplier than interventions which also absorb default risk. Absorbing default risk requires a larger subsidy, but the additional investment generated — the extra production that results from eliminating real risk — does not justify the higher cost.

For credit guarantees, the picture is more nuanced. Under financial frictions that raise borrowing spreads, the non-de-risking guarantee similarly dominates for practically all levels of default risk. But under credit rationing — where borrowers face hard limits on how much they can borrow regardless of the interest rate — the full de-risking guarantee can achieve a higher multiplier when default risk is sufficiently high.

The practical implication is that full de-risking is rarely the right choice, and practitioners should resist the instinct to eliminate all risk from a project as a matter of course. The right question is not “can we make this project safe?” but “how much of the default risk, if any, does it make sense to absorb, given the nature of the underlying market failure?”

Guarantees or subsidised loans?

The paper’s second main result concerns which instrument to use. The comparison depends on accounting conventions — whether the cost of a subsidised loan is measured at its full contracted value or at its probability-weighted expected cost — and on the type of market failure being addressed. Under the expected-cost convention, which is standard in the economics literature and is the convention that I adopt, guarantees and subsidised loans carry equal expected costs for pure de-risking and for production externalities. Instrument choice in those cases therefore rests on operational and institutional considerations rather than on differences in fiscal efficiency.

For financial frictions, however, the guarantee consistently dominates. The reason is that a financial friction typically has a component that persists regardless of whether default occurs — the illiquidity premium, the due-diligence cost, the regulatory capital charge. A subsidised loan must compensate for this spread in every period the project does not default, whereas a guarantee is only triggered when default occurs. The guarantee is therefore structurally cheaper for addressing financial frictions.

For credit rationing, the guarantee dominates in most configurations, though the dominance is less clean and depends on the level of default risk, the severity of the constraint, and the productivity of the investment.

When blended finance does not work

Perhaps the starkest finding concerns the interaction between default risk and the effectiveness of blended finance. When the probability of default is high — the paper shows that multipliers typically fall below one once default probabilities exceed roughly 30 to 50%, depending on the productivity of the investment — subsidised loans simply do not have a catalytic effect. The public expenditure required to bring private investors to the table outweighs the private investment mobilised.

This is not an argument against intervention. The social returns to investment in fragile or conflict-affected states may be very high, and closing an investment gap may be worth doing even when the multiplier is below one. But it is an argument against using blended finance in that situation. When the multiplier falls below one, the right response is to reconsider the instrument, not necessarily the intervention.

A practical rule of thumb

The paper’s three results distil into a simple decision hierarchy for practitioners. The first step is to diagnose the nature of the market failure — whether the distortion lies in the real economy (a production externality) or in the financial system (elevated borrowing costs or credit rationing). Production externalities call for subsidised loans, not because they are cheaper than guarantees in these settings but because guarantees are often simply ineffective when a project carries low default risk: with nothing to insure, the guarantee mobilises nothing. Financial frictions call for guarantees, which address the underlying distortion more efficiently than subsidies under both accounting conventions.

The second step is to decide whether to absorb default risk. The general presumption should be against full de-risking. It is warranted only in the narrow case where credit rationing is the dominant friction and default risk is high enough that eliminating it unlocks a large increase in borrowing capacity. In all other cases, targeting only the market failure — and accepting that some default risk remains — achieves a better multiplier.

References

Aydın, H, Ç Bircan and R De Haas (2024), “Blended Finance and Female Entrepreneurship”, CEPR Discussion Paper No. 18763.

Chari, A, P B Henry, Y Lee and P Mauro (2025), “Financial Returns to Equity Investments in Infrastructure in Emerging-Market and Developing Economies”, NBER Working Paper 34537.

Claessens, S and S Kapoor (2026), “Bending the Climate Change Curve by Blending Finance: What is the Real Potential Value-Added of Guarantees?”, CEPR Discussion Paper 21330.

Flammer, C, T Giroux and G Heal (2024), “Blended Finance”, NBER Working Paper 32287.

Panizza, U (2026), “The Catalytic Effect of Blended Finance”, CEPR Discussion Paper 21387.